What Is A Pfic? Passive Foreign Investment Companies

-

-

Important issues relating to the investment in foreign mutual funds

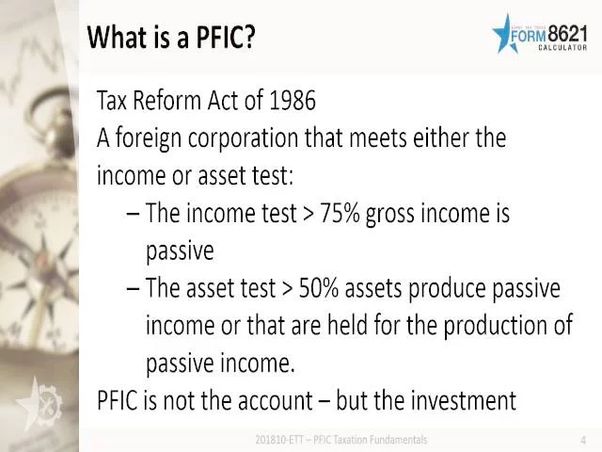

The literal definition of a Passive Foreign Investment Company is a foreign corporation of which at least 75 per cent of the income earned is “passive” i.e. dividends, interest etc., or 50 per cent of the assets held by the corporation generate passive income.

In practice, a PFIC is an investment in a foreign (non-US) mutual fund, OEIC, ETF, unit trust or other investment vehicle incorporated as a non-US company (or trust, which the IRS deems to be an investment company). Virtually every foreign mutual fund is a PFIC, and doubtless many US taxpayers living abroad will have invested their assets into mutual funds in the country they are living without any idea of the PFIC rules. Furthermore, their financial advisers may have invested them into PFICs as they have been historically unaware of the issues regarding investments for their US-linked clients.

Originally enacted in 1986, PFIC legislation was designed by Congress to discourage the use of foreign corporations to delay or reduce tax on financial assets, which can provide a significant tax advantage to investing in foreign mutual funds over domestic ones.

PFICs are often referred to as “toxic” assets because of the following issues for individual US taxpayers:

The PFIC legislation includes punitive tax and interest treatment relating to the both the income and the sale of the funds which—in theory—can result in an effective tax rate of over 100 per cent on the gains from the funds. The treatment essentially spreads out any gains made in the fund to the entire period you have held it; tax is then calculated at the highest marginal tax rate in each year of holding and then interest calculated on the tax due; and Since Tax Year 2013, all US taxpayers are required to report detailed information pertaining to the taxpayer’s holdings in the year of PFIC assets on the newly instituted Part 1 of Form 8621. This means that the taxpayer is required to file a separate Form 8621 for each separate fund you held during the year even if there was no income generated by the fund or you did not sell it. Thankfully, the Treasury have issued regulations specifying an aggregate de minimus value of a shareholder’s PFIC reporting requirement on Part 1 of Form 8621 of $25,000 for single taxpayers (or married filing separate) and $50,000 for married filing joint. If the total value of your PFICs are below the applicable amount you do not need to declare them on Part 1 of the Form 8621. However, Form 8621 will still need to be filed if the asset was sold during the year or you received what is referred to as an “excess distribution”

Join the Discussion